Mortgage rates in the Denver metro area have shifted in 2026, creating a very different environment for homebuyers compared to the volatility of recent years.

The market is no longer defined by extreme spikes or sudden drops.

Instead, buyers are navigating a more stable—but still expensive—housing landscape where understanding your total cost matters more than ever.

In practical terms, today’s mortgage rates mean buyers are paying more money over time for the same home than they would have just a few years ago.

At the same time, reduced competition and improved inventory are giving buyers more room to negotiate and make smarter financial decisions.

That combination is what makes 2026 unique.

Knowing what you can afford, how rates impact your monthly payment, and how to structure your loan properly allows you to move forward with confidence instead of uncertainty.

For buyers planning a move, purchase, or investment in Denver, this is not just about interest rates—it is about understanding how to make your money work in a changing market.

If you’re planning a move based on affordability, working with experienced Denver movers can help you transition efficiently once you secure your home.

How Much House Can You Afford in Denver in 2026?

Buying a home in Denver can feel competitive, especially when rates, inventory, and home prices are all shifting at the same time.

The game is about managing the new normal of home loans, working with mortgage lenders, and evaluating what’s best for your family.

After so many years of serious swings, the rates have finally begun to level off.

This is allowing borrowers to plan their financing with more confidence.

If you’re comparing affordability changes, see our breakdown of 2024–2025 Mortgage Rates in Denver.

The market has moved into a more predictable phase after years of elevated prices and high borrowing costs.

Here’s what you can expect:

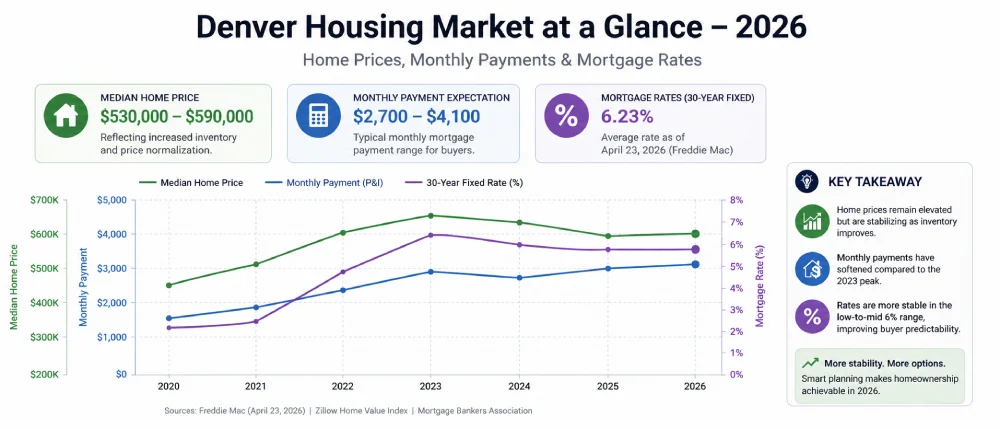

- The Denver metro area is now tracking above the national average, with the median home price around $530,000 to 590,000. This range reflects increased inventory and price normalization rather than a market decline.

- Monthly mortgage payment expectations have begun to soften, with many buyer scenarios falling between $2,700 and $4,100.

- Mortgage rates are generally sitting in the low-to-mid 6% range, with Freddie Mac reporting the average 30-year fixed rate at 6.23% as of April 23, 2026.

For many prospective buyers, the combination of rate stabilization and less competition in 2026 creates new opportunities to negotiate better deals.

How Colorado Mortgage Rates Have Changed in Recent Years

2026 marks a transition from a seller-driven market to a negotiation-driven market.

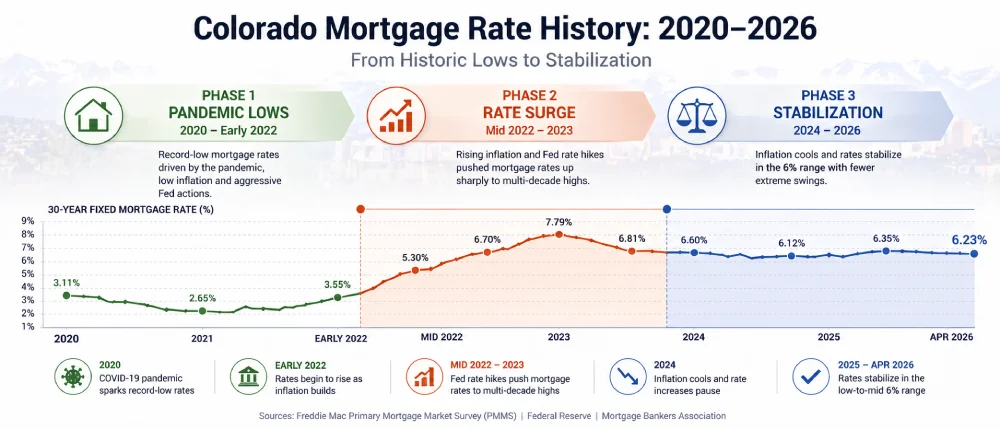

Colorado mortgages have fluctuated widely over the past several years, moving from pandemic lows to extreme highs in the years that followed.

Knowing how these changes affect your down payment, interest rates, and borrowing capacity helps you plan if you are considering your first or a new home in the Denver area.

Pandemic-Era Mortgage Lows

When COVID-19 shut down the world, mortgage rates in Colorado and across the US fell sharply.

These were among the lowest in modern history due to a slowdown across the entire economy, prompting the Federal Reserve to further decrease the interest rates to maintain growth.

Many buyers used this timing to their advantage, with a ton of homebuying activity and refinancing happening during this time period.

Rate Surges During Inflation

Once inflation began accelerating rapidly in 2022, mortgage rates rose steadily, increasing costs across the board for homebuyers.

This made the overall homebuying process a lot more difficult.

This was when interest rates first rose above 6%, doubling from previous years.

Gradual Stabilization Heading Into 2026

After such an intense increase during the peak of inflation following the impact, mortgage rates have finally begun to stabilize.

These conditions are expected to persist, and even though rates remain higher than in the past, we expect fewer extreme fluctuations.

As inflation cools, the housing market in the Mile High is adjusting into 2026, putting things back into the buyers’ hands.

Economic Variables Influencing Colorado Mortgage Rates

Finding the best mortgage rate is important, but several larger economic factors also shape borrowing costs in Colorado.

- The Federal Reserve’s Mortgage Interest Rate Policy allows it to control the benchmark to better regulate inflation.

- When the Fed increases interest rates, borrowing costs typically rise.

- When rates are lowered to enhance economic activity, mortgage rates often follow with more favorable borrowing conditions.

- Inflation and mortgage rates are closely connected because lenders often price loans higher when inflation remains elevated.

- Strong housing demand in growing markets like Denver may also contribute to upward pressure on rates.

- When inflation begins to cool, mortgage rates may stabilize or gradually decrease.

- Population growth and migration to Denver, CO, will create significant change in the housing market landscape in the metro area.

- When additional buyers enter the market, lenders will adjust their offerings and rates to match regional demand and economic conditions.

- When migration increases, so does housing demand, which influences prices.

Affordability Among First-Time Homebuyers in Denver

The term ‘affordable’ is constantly changing and means different things to different people.

Still, affordability is the strongest consideration for those seeking to purchase their first home in the Front Range housing market.

Although interest rates are cooling, buyers still need to understand rate sensitivity, loan structure, and total cost of ownership.

For many buyers, affordability isn’t determined solely by the listing price, but rather by loan terms, down payment, and long-term financial certainty.

Make use of additional resources with the first-time homebuyers guide in Denver.

Below is a general idea of what to expect:

Mortgage Payments on Houses at $450k to $550k

These are considered entry-level homes for first-time buyers.

Monthly payments and average rates may vary considerably based on your loan application, payment assistance, credit history, insurance, and other factors.

- With a 20% down payment on a 30-year fixed mortgage, buyers looking at homes between $450,000 and $550,000 in Denver can generally expect total monthly payments from about $2,600 to $3,400, depending on the interest rate, property taxes, insurance, and lender terms.

- For a 15-year loan term, monthly payments are substantially higher because the balance is repaid faster. Buyers in this same $450,000 to $550,000 range may see payments closer to $3,500 to $5,000 per month with 20% down, depending on the final rate and total housing costs.

Buyers putting down 10% or 15% should expect higher monthly payments because the loan balance is larger and mortgage insurance may apply.

Houses at $600k to $700k

With a 20% down payment on a 30-year fixed mortgage, buyers purchasing between $600,000 and $700,000 in Denver can generally expect total monthly payments from about $3,500 to $4,600, depending on the final interest rate, taxes, insurance, and lender terms.

With a 15% down payment, payments may fall closer to $3,900 to $5,200 per month because the loan balance is larger, and PMI may apply.

With a 10% down payment, buyers should expect a higher monthly range, often around $4,300 to $5,800 per month, depending on mortgage insurance, credit score, and total escrow costs.

Houses at $750k to $900k

With a 20% down payment on a 30-year fixed mortgage, buyers purchasing between $750,000 and $900,000 in Denver can generally expect total monthly payments from about $4,600 to $6,200, depending on the final rate, property taxes, insurance, and lender terms.

With a 15% down payment, monthly payments may range from about $5,100 to $7,000 because of the higher loan balance and possible PMI.

With a 10% down payment, buyers should plan for payments closer to $5,700 to $7,900 per month, depending on credit profile, mortgage insurance, and total housing costs.

Mortgage Expectations for a House Between $950k and $1.5m

With a 20% down payment on a 30-year fixed mortgage, buyers purchasing between $950,000 and $1.5 million in Denver can generally expect total monthly payments from about $5,900 to $10,300, depending on the final interest rate, property taxes, insurance, and lender terms.

With a 15% down payment, monthly payments may range from about $6,500 to $11,600 because of the larger loan balance and possible PMI or jumbo-loan pricing.

With a 10% down payment, buyers should expect payments closer to $7,200 to $13,000 per month, depending on the loan program, credit profile, reserves, mortgage insurance, and total escrow costs.

Denver Housing Market Trends That Influence Mortgage Rates

Denver’s housing market influences interest rates and the cost of an average mortgage in 2026.

When the inventory shifts, so do demand and home prices.

These conditions together help determine the cost of a home and monthly mortgage payments.

Before you book your local movers, know what to expect in the market.

Inventory Levels

Housing inventory has increased significantly from previous years.

This creates less competition within the market and offers more power in negotiations.

However, this is not seen across the Denver metro area.

Certain areas like Highlands Ranch and Central Park see tighter inventory due to the strong demand for incoming families, and therefore, you may see higher home prices in the region.

Price Stabilization

After many years of appreciation, certain neighborhoods are finally stabilizing.

Highly sought-after areas like Cherry Creek and even Wash Park are seen as luxurious places, and while the home prices remain higher, things are not growing at such a furious rate anymore.

Buyer Competition

While the competition has decreased in 2026, there are still areas that will attract strong buyer attention.

Sloan’s Lake has been known as an up-and-coming neighborhood, officially a hotspot in Denver.

There are highly competitive offers, which can make it more difficult and lead to a heftier price tag.

Why the 30-Year Fixed Mortgage Remains the Market Benchmark

A 30-year fixed mortgage loan remains the most common loan type for homebuyers as it offers the most predictable monthly mortgage payment.

This kind of stability can make it easier for buyers to plan for the long term within their housing budgets and provide future protection against rising interest rates.

A fixed-rate loan provides homeowners with stable monthly payments, making it much easier to budget and plan for long-term housing expenses.

- Monthly payments remain consistent throughout the entire life of the loan.

- Borrowers are protected from prospective interest rate increases.

- This loan type allows homeowners to create a predictable long-term financial plan.

- Stable monthly payments make it easier to manage other expenses like property taxes, mortgage insurance, and maintenance.

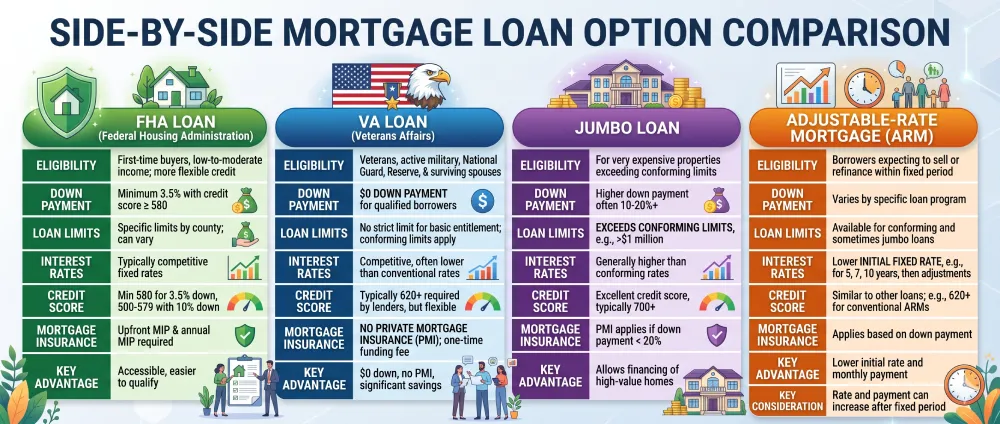

Other Mortgage Options Denver Buyers Should Compare

A 30-year fixed mortgage is the most common choice, but it is not the only option available to Denver buyers.

Depending on your income, down payment, credit score, and long-term plans, you may also want to compare FHA loans, Colorado jumbo loans, an adjustable rate mortgage, VA loans, and credit union lending options.

- FHA loans can help first-time buyers qualify with a lower down payment and more flexible credit requirements.

- VA loans, backed by the Department of Veterans Affairs, may help eligible military borrowers and veterans reduce upfront costs.

- A credit union may also offer competitive home loans, lower fees, or a more personalized loan application process than a larger bank.

- Colorado jumbo loans are often used when the purchase price exceeds conforming loan limits, which can happen in higher-priced Denver neighborhoods or when buying larger single-family homes and investment properties. These loans may require stronger income, a higher credit score, and larger cash reserves because lenders take on more risk.

- An adjustable-rate mortgage can start with a lower interest rate than a fixed-rate loan, but buyers need to understand the risk. Once the initial loan term ends, the rate can adjust, which may lead to higher monthly payments and more interest over time.

How Credit Score Requirements Affect Mortgage Rates

Even with market patterns, a borrower’s credit history and current score still matter.

A lower credit score often means a larger down payment, a higher interest rate, or stricter loan terms.

Every applicant is assigned to a credit tier based on their score, which determines their risk.

There are other factors, such as a minimum credit score, a debt-to-income ratio, and whether the loan falls within conforming loan limits.

- Buyers with a credit score of about 740 qualify for better mortgage options.

- Credit scores under 660 will result in higher interest rates, as lenders view the loan as high risk.

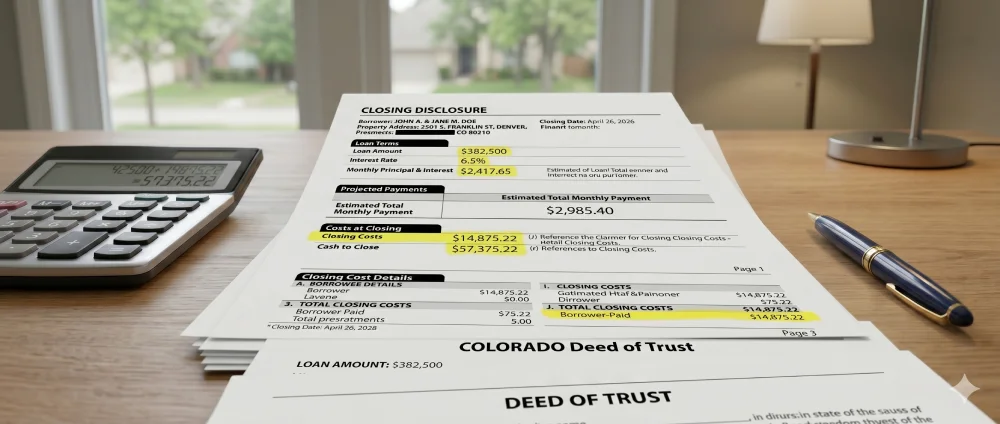

The Role of Closing Costs in Overall Mortgage Affordability

Closing costs are inevitably a part of every home purchase.

They can actually affect the property’s overall affordability.

Typical Closing Costs for Denver Buyers

Closing costs for Denver homebuyers typically range from 2% up to 5% of the home’s purchase price.

This means if you are purchasing a home for $600k, you can expect closing costs of $12,000 to $30,000.

These costs generally include lender fees, appraisal charges, title services, insurance, and other fees.

Planning ahead for these costs helps avoid surprises and ensures you are planning correctly for what is to come.

Below is a better picture of what you can expect to pay when buying a home in Denver:

Strategies to Reduce Closing Expenses

Seeking discount points and general closing-cost assistance can help buyers make their purchase much more affordable.

To reduce your closing costs, try the following strategies:

- Compare multiple lenders to find lower origination fees and better loan terms.

- Ask sellers if they are willing to contribute toward closing costs during negotiations.

- Look for lender credits that can offset some upfront costs in exchange for a somewhat higher interest rate.

- Review the loan estimate carefully to identify unnecessary or negotiable fees.

Home Equity Trends as Mortgage Conditions Change in 2026

Denver homeowners are in a great equity position even as those borrowing costs shift.

A reduced housing supply is supporting a change in property pricing, allowing equity to remain stable in 2026.

Here are the facts:

- Limits to the housing inventory further support home values across Denver communities.

- Buyers may be able to refinance later if rates improve.

- Denver homeowners are holding onto their property for longer periods due to the higher mortgage rates.

Future Predictions for Mortgages in Denver Moving Beyond 2026

Going forward, Denver can expect a slow but steady stabilization phase rather than high growth.

Forecasts point to a market shaped by economic forecasts, inflation trends, and demand.

- Rates may gradually ease, but buyers should plan for mortgage rates to remain near or above 6% unless inflation improves more significantly.

- Inflation inevitably remains one of the more significant players in what mortgages look like. Within the coming years, Denver homebuyers may see some relief if inflation continues to cool, but lower rates are not guaranteed, and monthly payments can remain elevated if home prices stay high.

- With all the new construction underway and that already built, there are more housing options, reducing buyer demand. While this doesn’t completely close the gap, with inventory growth, the market will become more balanced.

Tips for Dealing with Mortgage Rate Changes in 2026

Even as mortgage rates begin to decline in 2026, understanding how to respond to these changes can help secure the best financing terms.

- Lock Your Interest Rate at the Right Time: A rate lock may be helpful once buyers are under contract and comfortable with the quoted rate, especially if short-term rate movement could affect their monthly payment.

- Compare Multiple Lenders Before Choosing a Loan: Shopping around allows buyers to evaluate competing offers and may secure a lower interest rate.

- Improve Your Credit Profile Before Applying: A stronger credit profile can help borrowers qualify for better rates and loan terms.

- Plan Your Home Purchase Timeline Around Rate Trends: Monitoring mortgage rate trends can help buyers decide when to enter the housing market. Looking ahead to 2026, you are in a good place to start planning.

- Get Pre-Approved: This will help you understand what you are approved for and create a real budget, allowing you to make competitive offers when shopping for a home.

- Plan for More Than Just the Mortgage: Consider property taxes, home insurance, mortgage insurance, HOA fees, closing costs, and any maintenance or remodeling costs. This will offer a better picture of your initial and monthly housing expenses.

Planning Your Move Around Your Mortgage Closing Timeline

Once financing is secured, the next major step is coordinating your relocation.

Coordinating local or long-distance moving services in Denver means evaluating your timeline to ensure an easier transition.

Closing dates can often shift with inspections, approval of your loan documents, etc.

Preparing for your move shortly after accepting the offer is wise.

Aligning the relocation process with the closing dates can help you avoid additional temporary housing fees, a rush to pack, and last-minute scheduling challenges.

The cost of moving to Denver after buying a home can fluctuate if you are doing things at the last minute.

Understanding Moving Logistics After Buying a Home in Colorado

Once you have finally located and finalized the details for your primary residence, the next step is relocating.

Opting for professional movers can simplify the process, especially when you work with Denver VIP Moving Services.

This can offer specialized, experienced support for all moving coordination, so you don’t need to stress over it.

Frequently Asked Questions About Denver Mortgage Rates

Denver Mortgage Rates and Affordability in 2026: What Buyers Should Do Next

Mortgage rates in Denver have eased slightly in 2026, but affordability is still heavily influenced by home prices, loan structure, and total monthly cost.

Even small changes in interest rates can shift buying power, especially in higher price ranges.

For most buyers, the key is not trying to perfectly time the market, but understanding what monthly payment fits their budget and long-term financial goals.

Down payment size, loan term, and overall housing costs will ultimately have a greater impact than short-term rate fluctuations.

Once you’ve determined what you can comfortably afford, the next step is preparing for the move itself.

Working with a reliable Denver moving company can help streamline the transition and reduce stress during an already complex process.

By combining smart financial planning with the right moving strategy, buyers can navigate the Denver housing market more confidently in 2026.

Contact Eden’s Moving Services at (720) 370-3455 to request a free estimate for your move into your new home.